Ranking the eVTOL players

A conversation with Sergio Cecutta

☁️ Hi everyone, Robert here. Thank you and welcome to our new readers! If you haven’t subscribed yet, join the pioneering group of aerospace executives, investors, and deep tech operators who read Airframe.

The first time I tried writing for an online audience, it didn’t go well. I was 6 months out of college, working for a venture fund in the Middle East. I wrote a few articles for a local business journal that, when I read them now, still make me cringe. My “expertise” was in startups and venture capital, meaning I read everything coming out of Silicon Valley and repackaged it for the MENA region.

I built a small body of work with the local journal, which I presented to a larger outlet: Forbes Middle East. Forbes agreed to publish some of the new pieces I pitched them.

One of those articles was titled “The Top MENA Entrepreneurs And VCs To Follow On Twitter.” I thought it was a clever little piece that would drive clicks for the online version of Forbes. Although it was meant as an opinion piece, it read more like a definitive ranking endorsed by Forbes, e.g., the “Forbes 400” or “30 under 30.”

I got the clicks—and more than I bargained for. Some influential people were left off the list and the MENA Twitter community was not happy. I was chided for getting the list wrong and Forbes was criticized for publishing my article without “opinion” in the header.

In response to the criticism, Forbes made some quick changes: they softened the title by removing the word “Top,” and then pushed my writing to the opinion section. I commenced a brief apology tour on Twitter.

Through all of this, I learned a tried-and-true principle: people love a ranked list. A public ranking will always garner attention, create controversy, and lend the author some degree of power.

Sergio Cecutta may not have realized this when his consulting firm, SMG Consulting, started publishing the Advanced Air Mobility Reality Index. But now we all pay attention when his small team tells us how the eVTOL horse race is going.

Fortunately for us, Cecutta’s list is a hundred times more sophisticated than my Twitter power rankings. Supported by countless hours of research and travel, SMG Consulting assesses eVTOL developers based on five elements:

How much funding the company has received

The quality of the leadership team

The vehicle’s technology readiness

The vehicle’s progress in the certification process

The company’s readiness for full-scale manufacturing

Here is how the index has played out over time, with the most recent stats coming out just a few weeks ago:

Sergio is full of insights on the eVTOL market. It was a pleasure to sit down with him for this interview. Read our full Q&A below.

How did you end up in Advanced Air Mobility?

I am a veteran of Fortune 100 Corporations, having worked for Honeywell and Danaher. When I left Honeywell, I was in charge of all strategy and planning for the company’s commercial businesses. I went to Danaher to run some of their cleantech divisions, and then I founded SMG Consulting with some other folks. I hold a Ph.D. in Aerospace and an MBA.

What is your process for putting the AAM Reality Index together? What steps do you take before hitting publish?

I believe data is power. For all the companies that are in the index and companies that we want to put in the index, we make sure that we understand what they're doing. We study their latest milestones and we try to understand the second layer behind the public information. That is one of the reasons why we visit OEMs in person—there’s nothing like seeing with your own eyes what they're doing.

So have you visited most of the major OEMs and seen their offices?

Multiple times.

Setting aside people who actually work inside those companies, would you say that you know the OEMs better than anyone?

I don't know if I would go all the way to say better than anyone else, but we know them really well. No one is going to know them better than the people that work there because as much as they want to share, even under an NDA, there is always going to be some level of information that never leaves any of these companies. Nevertheless, we have a good grasp of all of the companies that we follow. There are a lot more that we follow that we're not ready to put in the index yet.

One of those companies must be more challenging to track than the rest: EHang. They seem to be more closed off than other OEMs in terms of their internal operations and certification process. How are you thinking about EHang in terms of where to put them on the AAM Reality Index?

The index is based on specific milestones that the OEMs have accomplished. EHang is a publicly traded company on the NASDAQ, so there is some level of information that comes out regularly. We take that information, and then we talk with their management to try to understand one level deeper what they're doing. So I wouldn't single out EHang as a complicated company to track. I don't think there is any single company that is too complex or one that we don't have an understanding of what's behind the curtain. If we did not really understand the company, we would not put it in the index.

EHang is not going to be everyone’s cup of tea, and it's not a vehicle that you can certify in Europe or in the United States, but at the same time, we should never underestimate the power of a large market like China.

Why do you think some people are very critical of EHang?

Some folks think that multi-copter solutions are not the most optimal solution for urban air mobility applications. At SMG Consulting, we think the answer is a little more nuanced. There might be better solutions, but you need to weigh that against how long it takes to certify those solutions, how much it costs to certify those solutions, etc. It's a little bit like if you are trying to show off when playing cards; if you keep all the cards close to the vest and it works out well for you, you look like a genius. But if it doesn't, you weren't even able to put a few cards down.

Vehicles are very market dependent. EHang is not going to be everyone’s cup of tea, and it's not a vehicle that you can certify in Europe or in the United States, but at the same time, we should never underestimate the power of a large market like China and what can come out of it.

I want to ask you about another OEM that's near the top of your index: Volocopter. The criticism I hear them is that they'll get to market, but the product isn't very useful. I'm curious: how are you balancing the commercial readiness of an eVTOL versus whether it is an economically viable product?

I don't think that there is a scientific way to identify whether a certain vehicle is a good product. I think even Volocopter has acknowledged publicly that VoloCity is just their first product and will be followed by more sophisticated products.

I’ll stress that it's a big deal to go to market. We're not talking about doing a GA aircraft where there are companies in countries all over the world that can do it. These are tiny miracles of technology. It’s the first time that something this small is a triplex fly-by-wire. We used to call it part 23, now it's Powered-Lift, but it doesn't matter. We’ve never had something so small with such complex controlled systems. In most of these vehicles, when you move an inceptor, you really don't know exactly what the airplane is doing. If you issue a command like “I want to climb,” the airplane decides what it means to climb. It's not like the old school system where you have an elevator and aileron—this is a lot more complex.

So if you look at Volocopter, I think it would be it would be restrictive just to look at the VoloCity; they are building a family of products.

So when it comes to Volocopter, I don't think we should underestimate being one of the first to market. We're writing the rules of the game while we drafting the players, building the stadium, and getting the fans. There are a lot of “unknown unknowns,” and whoever is first to market will be able to answer a lot of these questions. And they're not going to publish a big white paper that says, “Hey, learn from my mistakes!” No, they're going to keep a lot of things close to the vest. One other thing worth mentioning is that we’re seeing the first OEMs get a lot of involvement from the authorities because it's the first time they’re doing it.

So if you look at Volocopter, I think it would be it would be restrictive just to look at the VoloCity; they are building a family of products. The VoloRegion, for example, is an aircraft that's significantly more capable: it has more range, more speed, and can carry more passengers. So we look at all of these through the lens of the strategy that the specific OEM has. So if it was just one product, that is one thing, but when you have a family of products, it’s something bigger.

Every time you release a new Reality Index, individual OEMs and infrastructure players move up or down the rankings. Do you ever get anyone who's upset by the changes? How do you deal with that aspect of maintaining a ranking for AAM?

It's the old paradox that if you're on the list, nobody notices, but if you’re not on the list, everyone notices. So usually when people move up, we don’t get a “this is awesome!” We’ve built this to be completely data-driven. Our opinion doesn't exist; it's just based on the milestones. So when companies have said, how can we climb? We say, just do your job, and you’ll go up. No one has complained, and we always have a good explanation for any movement. The OEMs themselves are not surprised by the rankings. It's all based on the information that they've released or information that we have. And the way that we build the index itself, it's built in a way in which we can incorporate non-public information without disclosing it. The important thing for us was to take out the element of “I think”. Data is data, and that is what this index is all about.

Have you ever seen an industry come out of thin air like what we're hoping will happen with eVTOL? It’s a small community in which everyone knows each other, and in theory, we're going to be able to produce an industry out of nothing (of course, building upon decades of research and development). Have you seen that happen successfully anywhere else? And how much of that effort is going to be the product of collaboration versus competition between players?

Let me first answer the latter part of your question. Aerospace is an industry that needs collaboration. It is a very regulated industry for very good reasons. It's not easy to put stuff up in the air and keep it in the air safely. And so if you went to talk to every OEM, they would tell you that right now is not the time for competition; it’s the time to all work together, understand all of the different pieces, all the different regulations, etc. That is the reason why you see a G-1 Certification Basis published, and then everyone wants to talk about it. But it's not from a desire to handicap competitors, but rather to learn so that when it comes to be their turn, they can succeed. So competition is always important, but right now is not the time of competition. The time of competition will come. We all know that there are way too many companies in the industry, and that’s just not going to work. But now is the time to cooperate.

The OEMs themselves are not surprised by the rankings. It's all based on the information that they've released or information that we have.

When it comes to an industry coming out of nowhere within aerospace, it hasn’t happened many times, and there have been many false starts. But commercial space is one that has worked out. It’s dominated by SpaceX, and a friend recently commented that they’ve taken the mystery and intrigue out of space launches because there is almost one launch a week. It's no longer, “Let’s go to Cape Canaveral, maybe we’ll see a rocket!” Now you’ll definitely see one, if not multiple launches in a week.

But if you look at the aerospace industry, some like to compare eVTOLs to the very light jet market, but I think the fundamentals are completely different between the two. You had one aircraft and one client, but in this case, we're talking about many competitors and a lot of capital. AAM is an industry that has revitalized aerospace. Articles from five years talk about the issue of most of the workforce starting to retire within the next 15 years; we had that problem because we weren't able to spark the interest of the younger generation. Now, walking into the office of any one of the eVTOL OEMs, I am definitely one of the oldest people in there. Part of me doesn't like it, but I do like it for the industry.

Additionally, there is also a lot of attention at the national and international levels—they’re all doing what they need to be doing in order to stand up this market.

AAM is a very broad term, right? AAM is essentially everything that it's not already out there flying. If it’s not GA, a helicopter, or air transport, then it’s advanced air mobility. AAM has many different use cases. Some use cases will present themselves first, some use cases will grow faster than others, and ultimately, there will be new ways of moving people. Short-distance movements are really interesting. For a long time, we’ve thought about moving people far or moving people fast, but until recently, we never thought about moving people short distances in the air.

You mentioned that now's the time for collaboration. Is Joby more closed off than the other OEMs, and are they doing the industry a disservice by not being more collaborative?

I wouldn't say Joby is closed off. Joby participates in every single committee that I'm on. They are on many committees that people are not even aware that they are on. They are somewhat closed off in terms of sharing details on their development. But at the same time, that is a strategic choice and a communication choice. But when it comes to working with the industry, they're working with the industry like everyone else, if not more than many other folks that maybe are more public. I can tell you that there are Joby people in every single meeting that I go to, it’s just that they may not publicize it.

What can you tell me about Eve’s progress

Eve is backed by Embraer, and Embraer really owns, according to what you read, between 80% and 90% of the company. Except for their name, they are basically a division of Embraer.

And Embraer knows how to certify products. It's a little bit like Airbus; no one is doubting that Airbus can build an eVTOL. It is when they want to do it, not if they can do it.

So Eve has an advantage there. And they're being very conservative. They just opened their new headquarters in Melbourne for Eve. They are taking all the right steps in terms of not being pressured to be one of the first. And again, they have Embraer behind them, which is not a small thing. And Eve might be the only product that Embraer comes out within this decade.

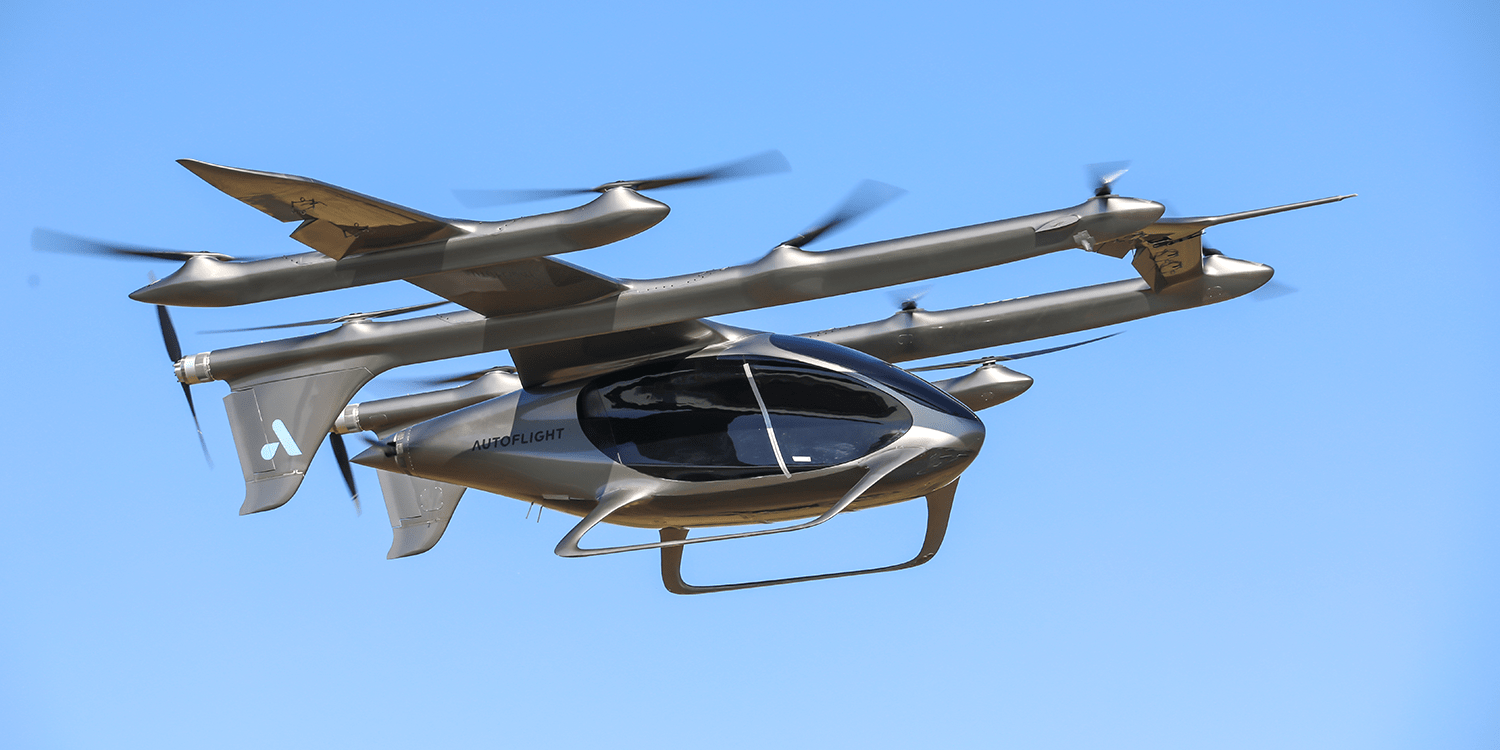

Autoflight had a big jump in the index. What is the single biggest factor contributing to their rise?

Flight time. There is no substitute for flying. They have over 1,600 hours of flying. There are only three companies that have flown as much as them: Volocopter, Joby, and Beta. Autoflight is the only company to have transitioned as many times as Joby. If you think about it, Volocopter doesn’t transition and Beta hasn't transitioned yet. They have done more than 400 transitions and so it’s becoming a non-issue. And transition is always a big deal. The aircraft is basically doing crawl, run, walk, and it's not easy to do. They have gathered so much expertise. They have not communicated publicly as much as other companies about their progress, but they are probably up there as far as the amount of hours that they’ve flown.